A client files a claim after a flood damages their warehouse. The insurer denies it: flood is excluded on page 14 of the policy. The client's response is predictable: "Nobody told me about that exclusion."

The insurer points to the signed policy. The client's attorney points to the fine print. And the regulator opens a complaint file.

This scenario repeats across every insurance market in the world. The policy was signed. Whether the client read the exclusions - or understood them - is unknowable. And the cost of that uncertainty falls on the insurer: complaint handling, legal defense, regulatory scrutiny, and occasionally, a court ruling that the exclusion was not adequately disclosed.

The legal principle is clear. Courts recognize that there can be a big difference between reading a policy and understanding its terms. The burden of making coverage exceptions and limitations conspicuous, plain, and clear rests with the insurer. A signature on the policy proves the client received a document. It does not prove they read the section that matters.

The Complaint Problem: Communication, Not Misconduct

Insurance regulators worldwide report a consistent pattern: the majority of complaints against insurers are not about illegal behavior. They are about misunderstanding.

The distinction matters. When a client complains that their claim was wrongfully denied, the regulator investigates. If the denial was lawful - the exclusion was in the policy, the client signed it - the complaint is technically unfounded. But the insurer still spent resources responding to it: staff time, legal review, documentation, and the reputational cost of appearing in complaint statistics.

The root cause in most cases is not bad faith by the insurer. It is insufficient communication at the point of sale. Complex policy language, rushed explanations, and checkbox acknowledgements create a gap between "policy delivered" and "exclusions understood."

This gap generates complaints that are expensive to handle and impossible to prevent with current documentation methods. A signed application proves delivery. It does not prove comprehension. And when the regulator asks "how did you ensure the client understood the exclusions?" - the answer is usually a signature on a form.

The pattern holds across markets. In regulated insurance markets, complaint rates for communication-related issues consistently exceed those for actual legal violations. The insurer acted correctly. The client genuinely did not understand what they signed. Both statements can be true simultaneously - and the cost falls on the insurer regardless.

What the Law Requires - and What It Leaves Undefined

Insurance regulation increasingly requires insurers to demonstrate that clients were informed before signing. The specific requirements vary by jurisdiction and insurance class, but the direction is consistent: disclosure obligations are expanding.

Pre-contractual disclosure laws require insurers to provide clear, accessible information about the insurance product - including exclusions, limitations, and grounds for claim denial - before the client signs. Some jurisdictions go further: for life insurance and long-term products, the insurer must obtain written confirmation that the client reviewed the information and has sufficient understanding to make an informed decision.

The EU's Insurance Distribution Directive (IDD) establishes a framework where distributors must act in the best interest of the customer, provide information in a comprehensible form, and identify the customer's demands and needs before proposing a product.

What these laws do not define: the format of "written confirmation," the method of proving "sufficient understanding," or the technology used to document that disclosure occurred. A paper signature satisfies the minimum requirement. But a paper signature on a 40-page policy does not answer the question courts increasingly ask: "Did the client actually read the exclusions?"

This is the gap. The law requires disclosure. It does not specify how to prove it happened. And the difference between "we gave them the document" and "we can show they read page 14 for two minutes" is the difference between a contested complaint and a closed one.

How Reading Analytics Close the Gap

Page-level document analytics - the same technology used to track whether investors read pitch decks or employees read security policies - can transform insurance disclosure from a checkbox to an evidence trail.

The mechanism applies directly to the insurance workflow:

- At the point of sale, the agent or online platform shares the policy document - or a key exclusions summary - via a tracked link. The client receives it on their phone, tablet, or computer

- The client reads in a browser-based viewer. No app download, no account creation. The document opens immediately

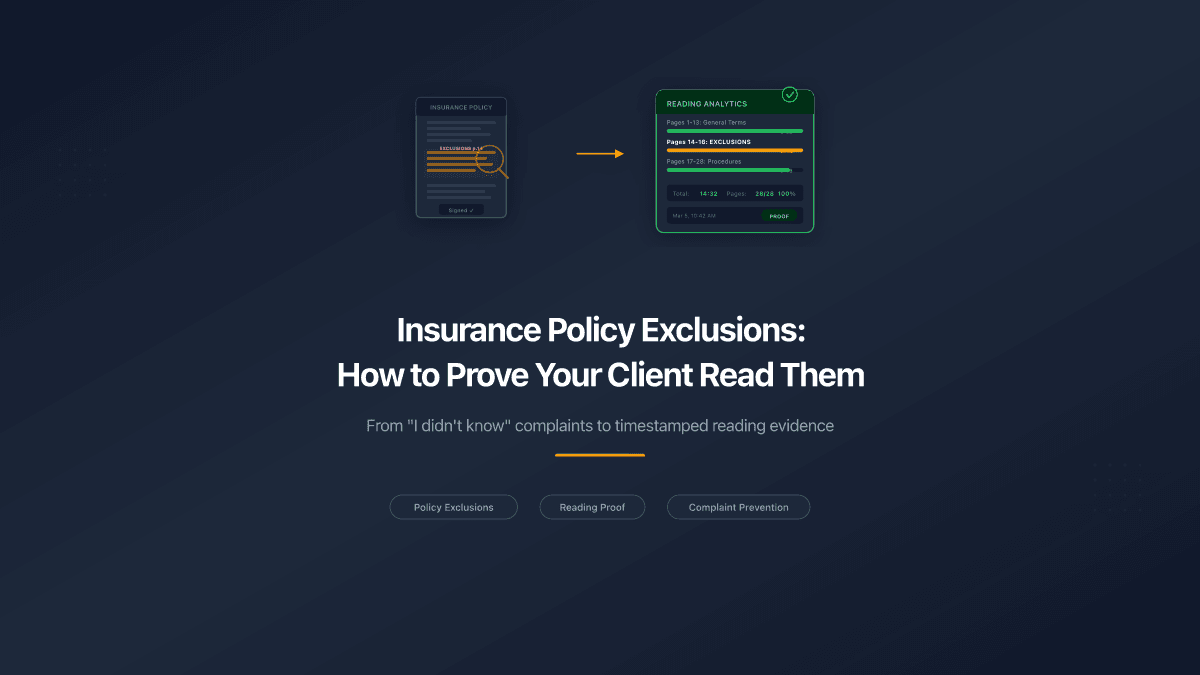

- The analytics engine records the session: which pages the client viewed, how long they spent on each page, whether they reached the exclusions section, and whether they returned to review specific provisions

- The insurer retains a timestamped record: "Client viewed the policy on March 5 at 10:42 AM, spent 12 minutes total, viewed all 28 pages, spent 2 minutes 14 seconds on pages 14-16 (Coverage Exclusions)"

Three outcomes are possible, and each tells a different story:

The client read the exclusions. The record shows they spent meaningful time on the relevant pages. When they later claim "I didn't know," the insurer has timestamped, page-level evidence to the contrary. The complaint is resolved at the first stage.

The client skipped the exclusions. The record shows they viewed pages 1-13 and 17-28 but skipped pages 14-16 (exclusions). The insurer warned. The client chose not to read. This is the digital equivalent of handing someone a document and watching them skip a section - documented and defensible.

The client did not open the document. The insurer has proof the document was delivered to the client's device. The client chose not to read it. This is stronger evidence than a signed form, because it proves delivery AND documents the client's choice not to engage.

In every scenario, the insurer's position is clearer than with a signature alone.

What Changes for Complaint Handling

The practical impact on complaint workflows is direct:

| Stage | Without Reading Analytics | With Reading Analytics |

|---|---|---|

| Client complains: "I didn't know" | Insurer produces signed policy. Client disputes reading it. Stalemate | Insurer produces reading data: "You spent 2:14 on the exclusions page on March 5." Complaint resolved |

| Regulator investigates | Insurer shows signature + policy copy. "Adequate disclosure" is debatable | Insurer shows page-level engagement data. Disclosure is documented |

| Court proceeding | Judge interprets whether signature = awareness. Often rules against insurer (contra proferentem) | Judge sees timestamped evidence of reading. Shifts burden back to client |

| Internal audit | No visibility into which clients actually read policies | Dashboard: 87% of clients read exclusions section. 13% flagged for follow-up |

| Agent training | No data on which policy sections clients skip | Data shows clients consistently skip Section 4. Agents trained to highlight it |

The last row matters for prevention. If analytics consistently show that clients skip the exclusions section, the insurer can redesign the document - shorter, clearer language, visual highlights - or train agents to walk clients through that section specifically. The data drives improvement, not just defense.

Reading analytics do not replace the duty to explain. An insurer that shares a 40-page policy via a tracked link and does nothing else has better documentation than one with only a signature - but the strongest compliance posture combines clear documentation, agent explanation, and reading verification. The analytics are one layer of evidence, not a substitute for good practice.

Life Insurance: Where the Law Already Requires Proof

Life insurance occupies a unique regulatory position in most jurisdictions. Because policies are long-term, involve significant financial commitment, and affect beneficiaries who are not party to the contract, regulators impose stricter disclosure requirements.

In several markets, the law explicitly requires the insurer to obtain written confirmation that the client reviewed the information and has sufficient understanding to make an informed decision. This goes beyond a general signature - it requires documented evidence of comprehension.

Current practice satisfies this requirement with a checkbox or a separate signature line: "I confirm I have read and understood the terms and exclusions." The client signs. The box is checked. But the same question applies: did they actually read and understand, or did they sign a form?

Page-level reading analytics provide a stronger answer. Instead of "the client signed a confirmation," the insurer can document: "the client spent 14 minutes reading the policy summary, viewed all sections including the exclusion schedule, and returned to review the beneficiary provisions twice."

For life insurance specifically, this is not a nice-to-have. It is the technology that matches what the law already requires - proof of informed understanding, not proof of signature.

Who Benefits

| Role | Current Challenge | With Reading Analytics |

|---|---|---|

| Chief Compliance Officer | Regulatory disclosure requirements growing; documentation is checkbox-based | Digital proof of client engagement per policy, exportable for regulatory review |

| Claims department | Complaint handling for "I didn't know" disputes consumes staff time | Reading data resolves disputes at first contact. Fewer escalations |

| Insurance agent/broker | E&O liability if client claims agent "didn't explain" | Proof that client received and read the exclusions document the agent shared |

| Underwriting | No visibility into whether clients read what they sign | Aggregate data: which policy sections are read, which are skipped |

| Product design | No feedback on policy document readability | Reading analytics reveal where clients disengage. Shorter exclusion sections, clearer language |

The EU and Global Direction

The regulatory trajectory is consistent across markets: disclosure obligations are expanding, and the evidence standard is rising.

The EU's Insurance Distribution Directive requires insurers to act in the client's best interest and provide information in a "comprehensible form." As EU candidate countries align their legislation, these requirements cascade to new markets. Insurers operating across multiple jurisdictions face a patchwork of disclosure rules - but the common thread is proof of adequate communication.

In markets with mature complaint frameworks - the UK's FCA, Germany's BaFin, Australia's ASIC - regulators explicitly examine whether the insurer's disclosure process was adequate. A signature satisfies the minimum. Page-level reading data satisfies the intent.

The insurers that build this evidence standard now will face future regulatory changes from a position of compliance. The ones that rely on signatures will discover the gap when a regulator or court asks the question that a signature cannot answer: "Did they read it?"

From Signature to Evidence

Insurance companies invest heavily in policy drafting: legal teams, actuaries, compliance officers, plain-language editors. The documents are precise. The exclusions are defined. The terms are clear to anyone who reads them.

The weak link is the last mile. The policy reaches the client. The client signs. Nobody knows if they read page 14. And when the claim is denied because of what page 14 says, the complaint begins.

A signature says "I received this document." Page-level reading analytics say "I spent 2 minutes and 14 seconds on the exclusions section at 10:42 AM on March 5." One is a formality. The other is evidence.

PaperLink tracks page-by-page viewing analytics for shared documents - including time per page, completion percentage, and tab visibility detection. Insurance companies use it to share policy documents and exclusion summaries with clients, creating a timestamped reading audit trail per policyholder. No app required - clients read in a browser on any device. Try it free.